| ||

| ||

| ||

| ||

| ||

| ||

|

Tuesday, May 21, 2024

Start Embracing AI

Tuesday, May 7, 2024

Help to Buy Scheme for frontline and essential workers - A Free Service

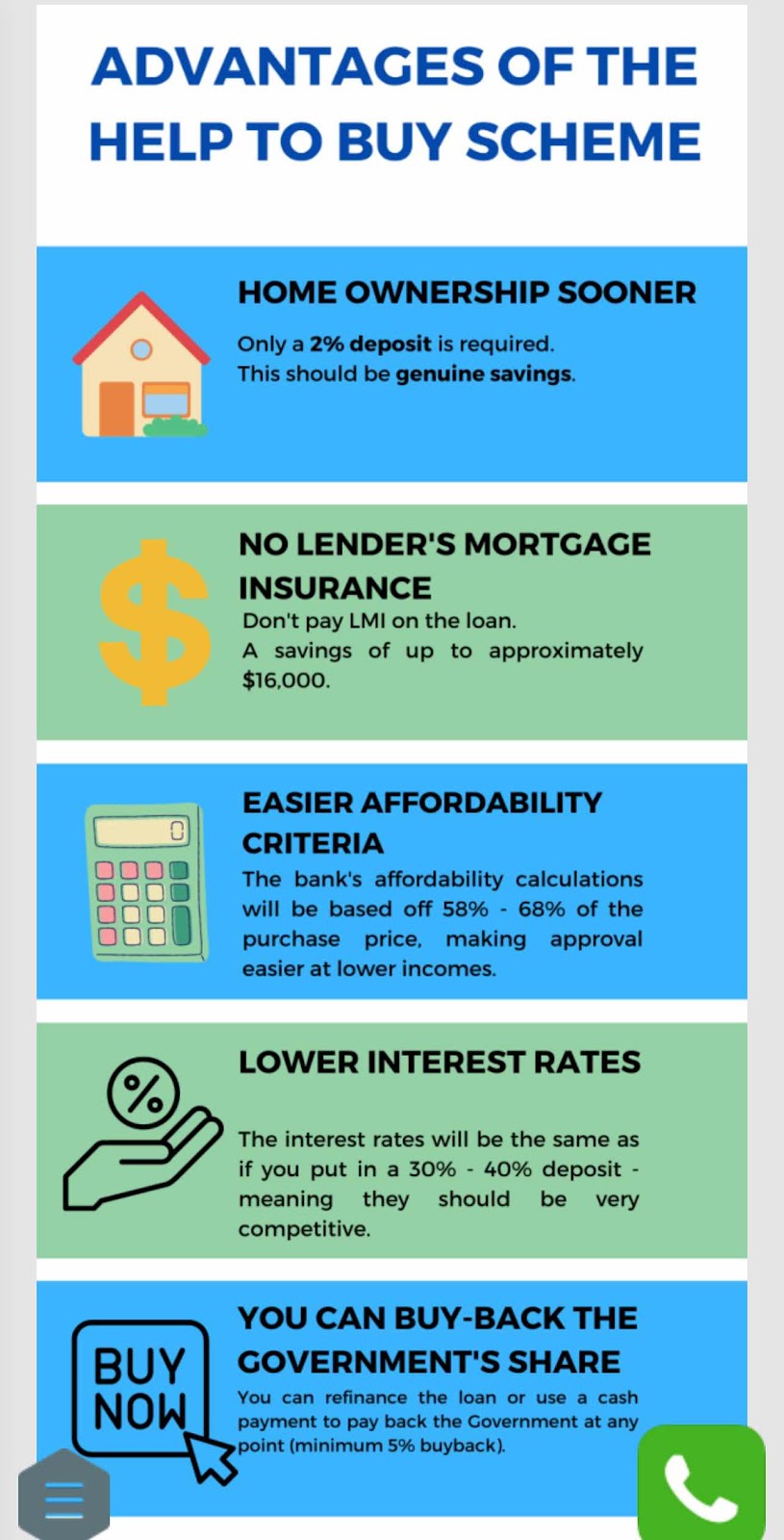

The Help to Buy Scheme is a Labor Government incentive which allows first home buyers (or second home buyers without a current property) to purchase with only a 2% deposit. The Government will then fund and own 30%-40% of the property.

Yes, you have the opportunity to partner with the government to buy your own home!!!

This will then allow the home buyer to get into the market quicker with a lower deposit, lower income, and lower ongoing home loan repayments. The applicant can then choose to buy the Government out at a later date.

Advantages of the Help to Buy Scheme

The main advantage is that it will get you into home ownership sooner. This can be broken down into a few

points...

Eligibility for the Help to Buy Scheme Australia

Expected eligibility criteria for the Help to Buy Scheme |

Income of less than $90,000 p.a. for a single applicant, or $120k for joint applicants. |

Must be purchasing a property to live in & must not currently own a property in Australia or overseas. |

Must be over 18 years of age. |

Must be an Australian Citizen. |

Must have a 2% deposit. |

There will only be 10,000 spots made available initially.

The Scheme is expected to run for 4 years, with 10,000 spots available each year, for a total of 40,000 spots.

These places will be released to individual participating States & Territories on a per capita basis.

Help to Buy Scheme: Expected start date

The Scheme is expected to start "Early 2024". Although, 01/07/2024 wouldn't be too surprising.

More details on the Housing Australia's Media Release Can be seen here , and Julie Collin's interview on ABC,

They should be releasing the Scheme in early 2024.

If you'd like to be kept updated, please sign up here and type waitlist

How to apply for the Help to Buy Scheme

You currently are unable to apply until it is released.

We will be watching the scheme carefully and contacting all interested applicants as soon as the scheme is ready for release.

If you'd like to be contacted when the scheme is ready, please register here.

We will use this information to keep you updated and to check your eligibility and prepare your submission.

That way we can get you one of the 10,000 spots ASAP and ensure you don't miss out.

Register here for a free service.

Saturday, May 4, 2024

How do you find a property in an area that grows faster than others?

There are many factors that determine what property to buy !!

One is location location location

Make sure that your area has consistent buyer demand!

But what research has shown is that some properties in the same location increases more than others!!

So, How do you find a property in an area that grows faster than others?

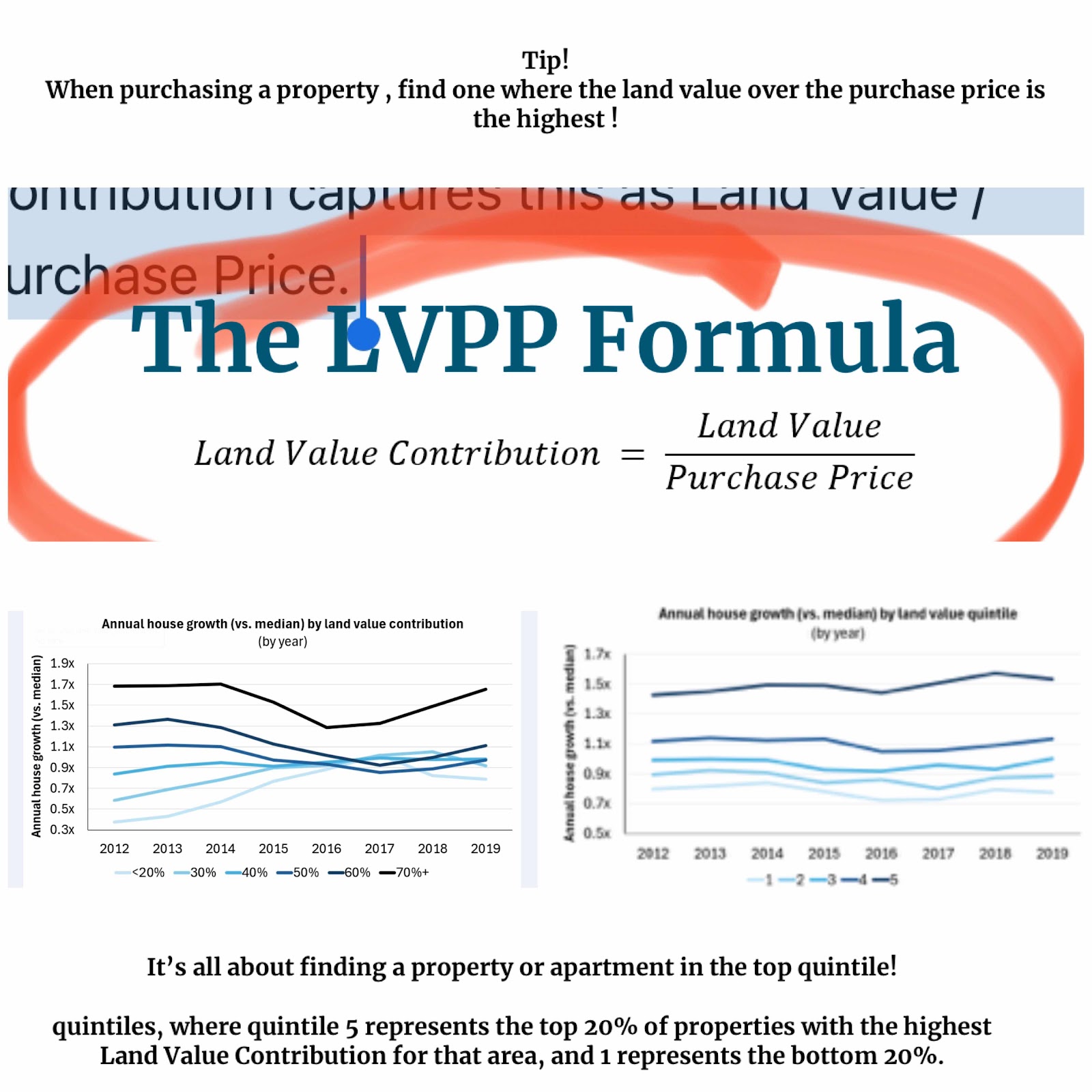

Easy says Robbie Baskin! - find a property where the LVPP is a 5 Quintile

Hmmmm 🤔🤔🤔🤔🤔🤔🤔🤔🤔

What is the LVPP?

And

What is a 5 Quintile ?

LVPP

The LVPP identifies how much of the purchase price is derived from land vs. the building.

The formula is pretty simple - find the land value of a house or unit and divide it by the purchase price!!

Land Value / Purchase Price.

Quintiles

A 5 quintile represents the top 20% of properties with the highest Land Value Contribution for that area, and 1 represents the bottom 20%.

Robbie Baskin of Frontya’s research shows that the LVPP formula is a strong indication of how your property will increase in an area compared to others!

So here’s the trick

Buy a house or an apartment where it's Land Value Contribution is in the top 20% for its area then chances are you'll achieve an annual property growth rate of 1.5x to the market.

Sunday, April 28, 2024

Property presentation in 2009 - what if.......... what will you be saying in 2035??

Saturday, April 27, 2024

Rents are skyrocketing, with tenants struggling to find accommodation

While the national vacancy rate was 1.0%, it was even lower in some capital cities:

To put that into perspective, a rental market is considered favourable to investors when the vacancy rate is below 2%; favourable to tenants when it’s above 3%; and neutral when it’s between those two benchmarks.

[Click here to book an appointment with Ivan Kaye]

And vacancy rates show no sign of increasing, because the population is growing strongly while the amount of rental housing is growing only modestly. In other words, demand is outstripping supply.

As a result, rental listings are attracting lots of tenant enquiries, and investors are finding it easy to fill their properties and justify rent increases. Rents across the country have jumped 9.4% over the past year, according to SQM.

Rents are likely to keep increasing while vacancy rates remain at such incredibly low levels.

Want to buy an investment property ? Click here to book an appointment with Ivan Kaye.

Wednesday, April 10, 2024

Growth gaining momentum for more affordable homes

An interesting article in the AFR on April 2 - saying units are rising at a faster rate than houses!

The growth rate for units and lower value houses have gathered momentum in the past three months, with values in the lower end jumping by 3.1 per cent, nearly five times faster than the upper end.

A main reason is that more downsizers seeking to reduce their mortgage are joining the buying frenzy! Says Ivan Kaye of BSI Finsnce.

A number of our clients are downsizing to reduce their debt due to increased interest rates .

Speaking to a financial adviser at Ark was a gamechanger for Jane (name and suburbs changed)

Jane , who was planning to retire in 8 years had built large equity in her home but was struggling with cash flow. She sold her large family home to relieve financial pressure.

“I just wanted to get rid of my mortgage and buy something smaller but comfortable and be able to sleep at night.” said Jane

Jane sold her house for $2.5 million, bought a unit for $1.5 million in Leichardt and put the money in Super - enabling her to be able to retire comfortably!

Tim Lawless - Research Director of Corelogic has said that demand for affordable homes has started outperforming the top end from last year - in each of the major capitals.

“With housing affordability becoming more challenging and borrowing capacity lower than a year ago, it’s no surprise to see demand being skewed towards the middle-to-lower end of the value spectrum,” Mr Lawless said.

“Originally, it was mostly investors and first-home buyers competing for those stock, but anecdotally at least, people are looking to reduce their debt, and maybe take advantage of the strong capital gains and cash out, downsize or move to a cheaper location where they can reduce their leverage.”

In Brisbane, house prices rose by an average of 7.4 per cent in Kingston, Riverview, Logan Central and Leichhardt in the Ipswich and Logan districts, where median values remained below $600,000.

Those were in stark contrast to the weaker performance in Brisbane’s upper end suburbs such as Hamilton and Ascot, where median prices reached $2.3 million and $2.5 million respectively. In the past three months, house values dropped by 3.7 per cent and 2 per cent respectively.

“A lot of downsizers are cashed up, so they can bid up and drive values higher in that segment of the market,”

“Depending on the suburb, big townhouses, a three-bedroom semi-detached house or apartments are highly sought-after by downsizers, making it harder for investors and first-home buyers to compete.”

Let me know if you are interested to buy or refinance your property by clicking here and contacting me at bsi finance

Source - Australian financial review And CoreLogic

Let me know if you are interested to buy or refinance your property by clicking here and contacting me at bsi finance

Sunday, April 7, 2024

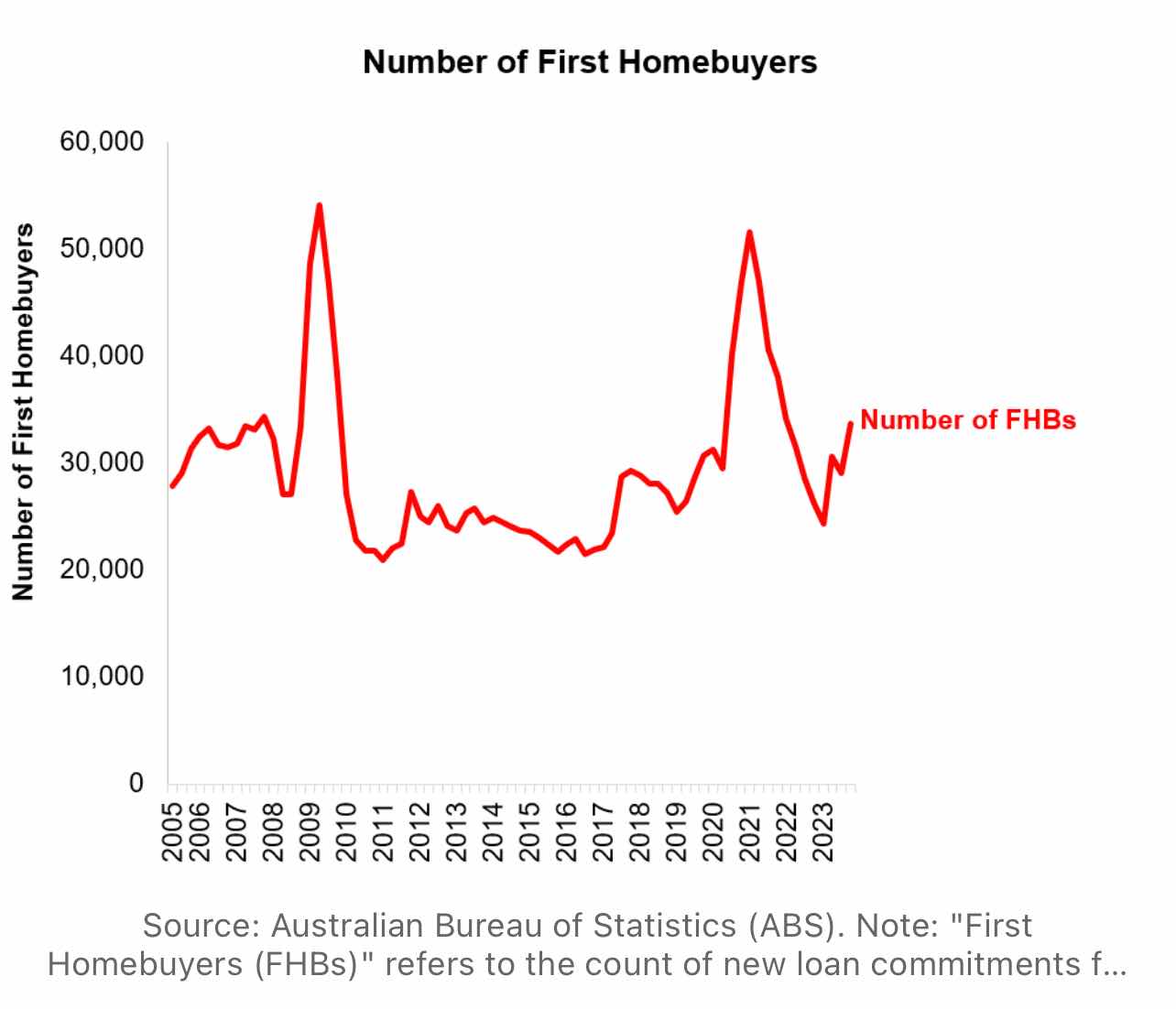

What’s the next Driver of First Home Property Buyers?

Over the past two decades, the quarterly count of first homebuyers has typically oscillated between 20,000 and 30,000.

Except for 2 periods

- The immediate aftermath of the GFC in 2009, and

- The COVID-19 lockdowns spanning 2020 and 2021.

Why?

- A dramatic reduction in interest rates? No.

- A withdrawal of property investors from the market? No.

- A willingness to take on high LVR lending? Definitely not.

The answer is Savings says Robbie Baskin from Frontya

Six months before these two distinct periods, a dramatic escalation in the savings rate was observed. The typical consumer was able to bring forward their ability to enter into the market with an adequate deposit. Once the savings rate stabilised, the number of first homebuyers went back to normal.

Household savings is clearly down and according to APRA, high LVR lending is down and property investor participation is up.

A 'deposit gap' is emerging - which will bring company’s like FrontYa to the fore - who will be able to help lower the 'deposit gap' through alternative funding schemes.

The new driver that seems to be emerging is the State and federal shared equity schemes .

Looking forward to see how this will change the landscape - enabling frontline workers to own their own homes by partnering with the government !