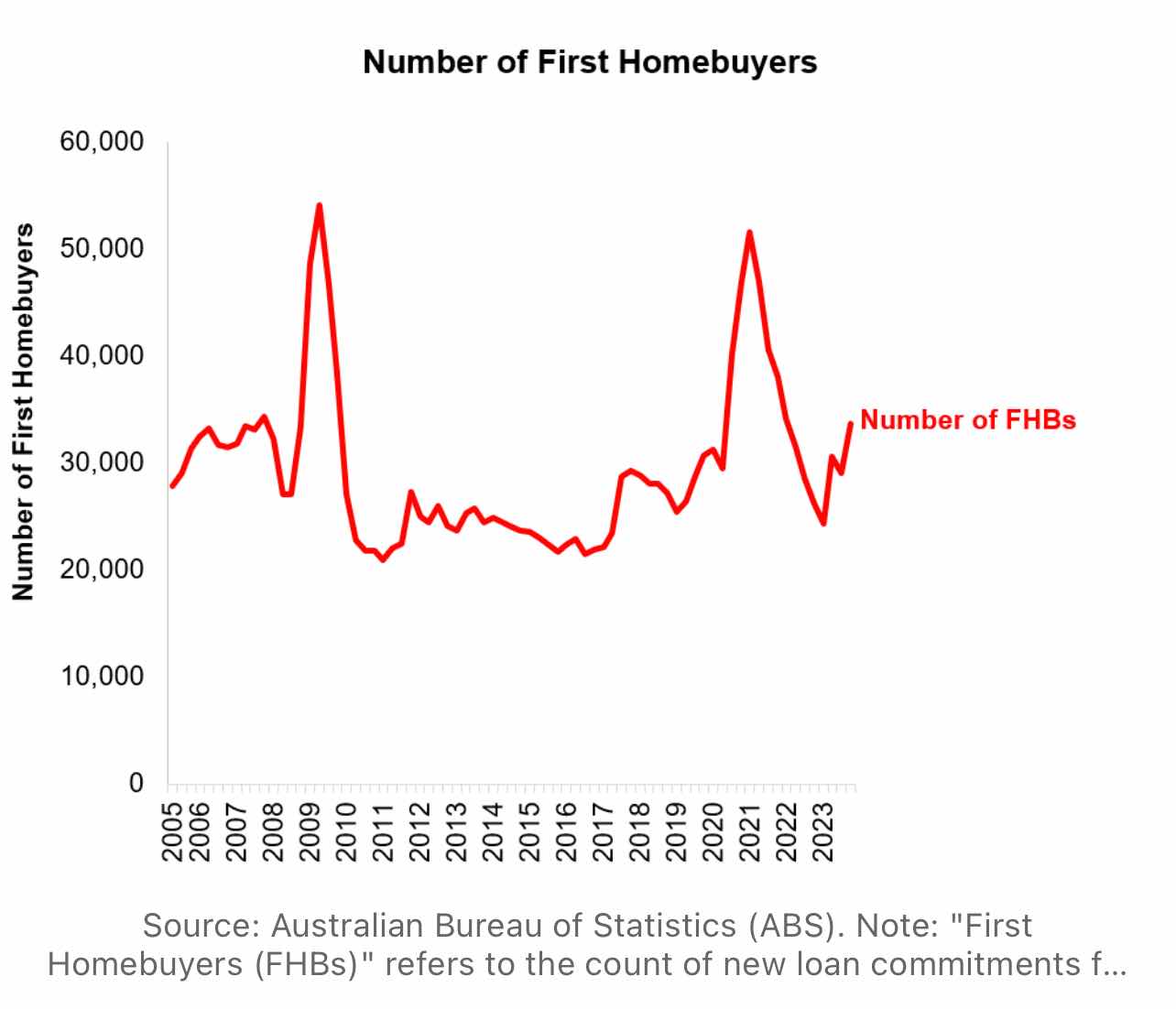

Over the past two decades, the quarterly count of first homebuyers has typically oscillated between 20,000 and 30,000.

Except for 2 periods

- The immediate aftermath of the GFC in 2009, and

- The COVID-19 lockdowns spanning 2020 and 2021.

Why?

- A dramatic reduction in interest rates? No.

- A withdrawal of property investors from the market? No.

- A willingness to take on high LVR lending? Definitely not.

The answer is Savings says Robbie Baskin from Frontya

Six months before these two distinct periods, a dramatic escalation in the savings rate was observed. The typical consumer was able to bring forward their ability to enter into the market with an adequate deposit. Once the savings rate stabilised, the number of first homebuyers went back to normal.

Household savings is clearly down and according to APRA, high LVR lending is down and property investor participation is up.

A 'deposit gap' is emerging - which will bring company’s like FrontYa to the fore - who will be able to help lower the 'deposit gap' through alternative funding schemes.

The new driver that seems to be emerging is the State and federal shared equity schemes .

Looking forward to see how this will change the landscape - enabling frontline workers to own their own homes by partnering with the government !

No comments:

Post a Comment