Tuesday, November 8, 2022

Sunday, November 6, 2022

Investing in Residential Property as an asset class

Alan Kohler and Evan Thornley talk about the investment elephant in the room !!!!

So what does the founder of Looksmart and a tech guru , Evan Thornley , know about property?

A lot , it seems

His company, LongView, now manages 4300 properties for individual investors and is also a national buyers’ advocate.

Thornley is about to disrupt this lazy giant!

Property and Gearing

Residential property and gearing …. A cocktail that has been given Australians exponential returns since 1926.

Solidly built properties, preferably on a rail corridor, have been an investor’s best bet for capital growth , as major city’s rapid population growth pumped up residential properties !

Total residential housing in Australia is $10 trillion, of which about $2.1 trillion is mortgage debt and $300 billion is in new developments. That leaves $7.6 trillion in equity in existing residential property, which is three times the size of the sharemarket.

And yet the $3.4 trillion in super funds don’t currently invest as there is not a liquid market and the risk/return equation makes it worthwhile.

It is certainly a big asset class – the biggest, in fact:

Research by Shane Oliver, of AMP, shows that the total return from residential property since 1926 has been 11 per cent a year – almost identical to the 11.3 per cent p.a. return from the sharemarket, but with much less volatility, so that’s a tick.

Shares vs Property and gearing (using OPM)

Real estate earns lower rental yields (2% than company dividends 6% (after Frankish credits ), but the gap is made up with negative gearing and capital gains.

The math

The magic formula for exponential returns - gearing and being able to afford rental repayments through net rent received and negative gearing!

An example of how the average property owner with a mortgage has made money since 1926!

Investor holds an investment property for 15 years at a net 3% shortfall (after tax 2%) - after 10 years property needs to increase by 30% in 10 years to breakeven .

No gearing

Let’s assume you purchased a property for $500k 15 years ago - and sold it for $1 million today.

Returns :-

After costs and negative gearing , your return would be $350k or 23k per annum (circa 5 %pa on an investment of $500k )

Gearing

Let’s assume you purchased a property for $500k 15 years ago - put down $200k deposit and sold it for $1 million today.

Returns :-

After costs and negative gearing , your return would be $350k or 23k per annum (circa 11.5% per annum )

So why don’t superfunds invest in property ?

- Rent returns are less than share returns

- Inability to Scale

- Low gearing policy

They need large investment vehicles, preferably with the ability to sell quickly, in large lumps, if they need to.

Enter Evan Thornley’s property fund

Evan Thornley puts business 101 into property

Customer Service

The goal :- To improve the rental experience for both tenants and landlords – to “dignify tenancy”, and provide a better service for investors, including guaranteed rent, where LongView takes the risk.

Investing in “solid older dwellings on well-located land”, as Thornley puts it, in the suburbs.

1. The bank of mum and dad and the Bank of Government - shared equity

One of the funds will be for long-term rental, and the other will invest alongside home buyers in a shared equity scheme….. much like the government is doing!!!!

In the shared equity arrangement, the fund wouldn’t own any part of the house but would provide up to a third of the deposit and stamp duty in return for a contract to share in the capital gain when it’s sold.

“Our shared equity clients are almost all migrants and children of migrants; sole parents and the children of sole parents,” says Thornley. “That is, people without the Bank of Mum & Dad.’’

2. Invest for rent through a REIT

The other fund will be a straightforward real estate investment trust that will create a suburban land bank of existing energy efficient houses for rent close to stations and shops so that large aggregated sites can be used for affordable housing in future.

The investment will be geared to rely on long term capital gains

Thornley says the initial interest in these funds will come from family offices and high net worth individuals.

Says Alan Kohler

Whether it’s Evan Thornley or someone else, the only way the superannuation pool can be mobilised for housing is if it can be pooled into funds that break down the super funds’ bias against it as an asset class and work as a decent investment.

Tuesday, November 1, 2022

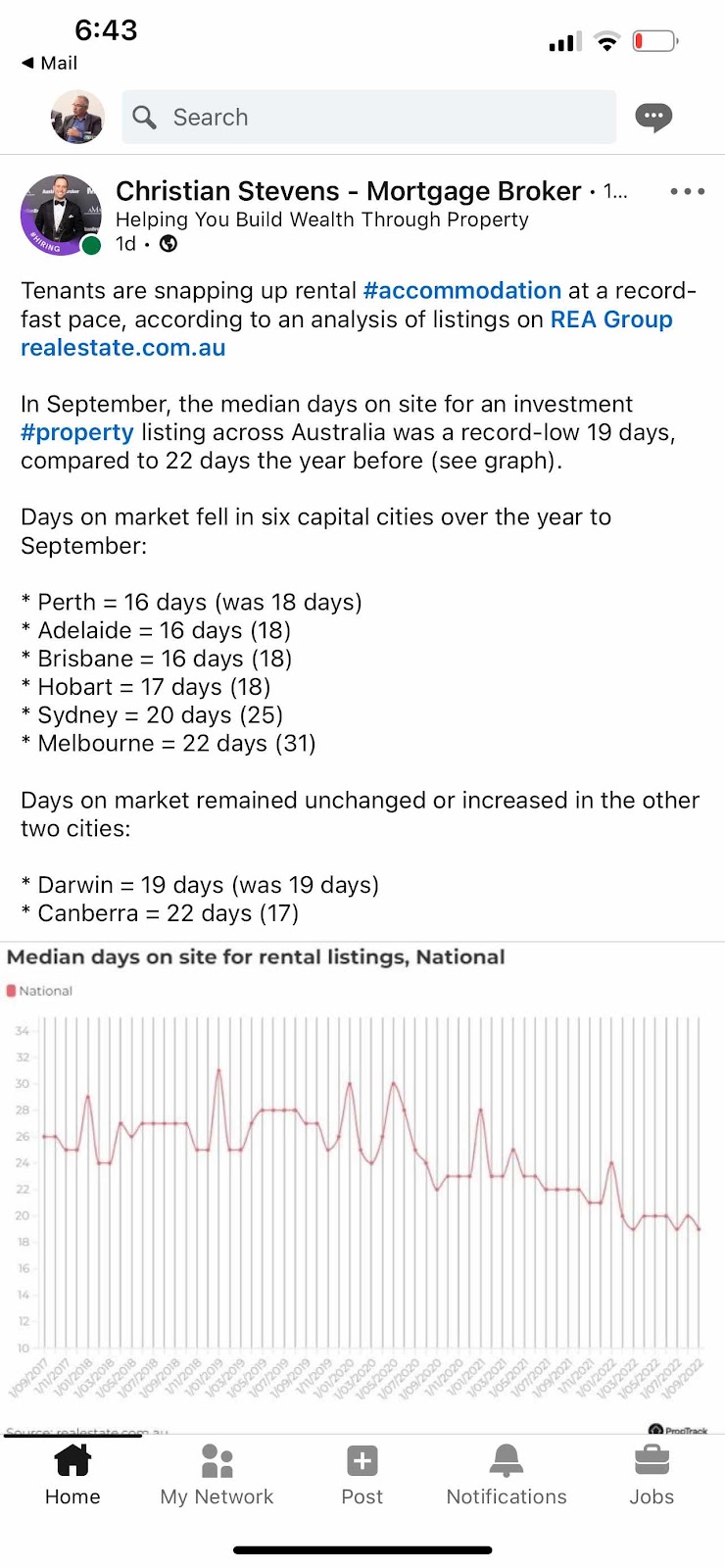

Are investment properties a good investment class?

An interesting post by Christian Stephens on the demand for rental properties !

As student migration into Sydney increase and the allocation of migration increase from 165k to 190k per annum ,

Together with the difficulty and bottlenecks of the supply chain for builders -

It seems that the demand for rental properties will increase !

Tuesday, October 25, 2022

Budget 22 - and focus on solving housing shortage

This budget delivered last night is all about addressing housing affordability over the long term by ramping up supply - say Treasurer Jim Chalmers

The Pain

- There is a shortage of property

- Property starts have been reducing

- Capacity constraints’ caused by material and labour shortages across the building industry are a constraint and needs to be solved

- Affordability is a major roadblock for many Aussies looking to enter the property market. According to the Australian Institute of Health and Welfare, 163,000 are on a waiting list for public housing, and Census data shows 116,000 are homeless.

- rents have surged by 10% nationally in the past year as demand soars and supply dwindles.

Towards a solution

A mission

“We want more Australians to know the security of decent housing and more Australians realising the aspiration of homeownership,” he said in a joint statement with the housing minister, Julie Collins.

A vision

“It’s more important than ever that we work together to ensure there is an adequate supply of affordable housing where it is needed – close to jobs, transport and other services.”

The federal government Budget has set an "aspirational target" to "build one million new well-located homes over five years from 2024".

A plan

The states and territories will be expected to "expedite zoning, planning and land release for social and affordable housing".

Labor’s flagship election promise – a shared equity scheme – aims to help more people enter homeownership with a smaller deposit and smaller mortgage.

The federal government's main role will be to create conditions that lead to more private investment from #superannuation funds and other institutional #investors.

“We have the world’s third-largest pool of capital in our superannuation system, which is hungry for investments that will deliver stable returns over the long term for the benefit of members.”

Housing supply and affordability is an important piece of the solution.

Under the new National Housing Accord:

* 10,000 of the one million homes will be financed by the federal government costing the budget $350 million. This was on top of the $10bn Housing Australia Future Fund, promised by Labor before the May election to build 30,000 new social and affordable housing properties in five years.

* 20,000 will be financed by the states and territories

* most will come from the market - superfunds and investors - we need to support them and remove barriers

* In 2020, the Victorian government announced a $5.3bn “big housing build” to fund 12,000 new social and affordable homes in four years. tripling the size of its Victorian Homebuyer Fund to $1.1bn

* The Queensland government, meanwhile, recently announced $2bn to deliver 13,000 social and affordable homes by 2027.

The challenges

Property prices are high

The median cost of a home in Sydney is still a whopping $1,053,131. A 20 per cent fall would only bring that down to $908,255.

In Melbourne, the median home value is $774,531. A 20 per cent fall would bring that down to $638,625.

The median price of a home in Brisbane is currently $746,017, while in Adelaide it’s $649,983.

The median home price in Perth is $558,879 and in Hobart is $705,079.

Property starts are low

According to the Australian Bureau of Statistics, about 985,000 new homes were built over the five years to March 2022, though the majority were completed before 2018-19.

Housing starts have been reducing due to COVID, weather , bureaucracy .

Treasury forecasts there will be about 180,000 housing completions on average across the next three financial years,

And yet there is a plan to bring in 190k immigrants a year

(Which is great)

Potential fixes

- “Removing tax barriers to institutional investment in new residential development projects such as build-to-rent could play an important role in tackling the undersupply of rental accommodation.

- “Improving planning regulations and removing inefficiencies that reduce approval times are key to this. So too is rezoning, releasing, and decontaminating land to enable more residential development,”

- freeing up ‘well located’ land, for example in and around train stations and TAFE campuses.

Support of frontline workers and others

Under the scheme, the government will co-purchase up to 40% of a new property (or 30% of an existing home) with an eligible buyer. Over time, the buyer could buy out the government, or pay out their share once the property is sold.

Help to Buy will be open to 10,000 Australians each year. Individuals earning less than $90,000 and couples earning under $120,000 could be eligible.

The government hopes to have the scheme up and running in the first half of next year.

For example, if a buyer purchased a $400,000 home with a 25% shared equity, they’d only make repayments on a $300,000 loan, minus any deposit paid up front. They will, however, need to cover the ongoing costs associated with owning a property.

This is already operating in several states, including Western Australia, South Australia, Tasmania and Victoria. And just weeks ago the NSW government proposed its own shared equity scheme.

From 1 October 2022, the Regional First Home Buyer Guarantee will help 10,000 buyers per year enter the housing market outside of the capital cities.

eligible applicants can purchase a home with a deposit of as little as 5%, with the government guaranteeing up to 15% of the purchase price.

Jim Chalmers

Saturday, August 27, 2022

7 keys to getting rich - slowly

Anthony Keane shares in the Sunday Mail on Aug 28 2023 the 7 keys to getting rich - slowly!

- Become an Investor - invest in real estate, property, your own business . Begin early - as time and compound interest is a magic source in wealth creation

- Leverage your investment with good tax effective debt - use other peoples money - where the interest you pay will be covered by the income earned from your investments and tax deductions - (make sure you have a great accountant, financial and mortgage broker who work together to maximise your opportunity

- Buy Property - it tends to double every 10-15 years - and easy to borrow against it at lowest interest rates

- Buy a business/businesses that you understand - most billionaires started with a business idea that worked - after many had failed before striking gold

- Diversify into other assets

- Seek passive income - where you earn income without having to work - such as dividends or rents

- Plan - write down your plan - and monitor your progress Don a regular basis

The IK formula steps simplified

Make sure that more money comes in than goes out on a monthly basis - and with that surplus

Buy low , Sell high with other peoples money - and do it regularly.

Don’t be afraid to take risks and fail until you succeed !

Sunday, August 7, 2022

Great article /podcast on Property in USA - very relevant to Property anywhere!

Molly Wood , JCAL , Redfin CEO Glenn Kolman and Divvey CEO Adena Hefets share what’s happenning in the USA real estate market !

Interest rates rising, housing unaffordable, , growth doubled since 2020!!!

Divvy - rent owner company - great way to purchase a property with the support of a capital base . Individual rents a property - buyer picks a home - part of rent to purchase - pays more to own 10pc over 3 years and then takes a mortgage

gets people into property faster

Redfin Online realestate - charges 1pc - using technology to sell a property

- Raising interest - massive impact - debt to income ratio - you can buy less home !! Banks only lend a percentage of what you earn !!

- Demand falling off a Cliff - currently down 30pc demand - inventory building up !

- Tail of many cities - hitting various regions differently

- IBuyers , institutions , builder mark properties down weekly

- People can’t buy - need to rent

- Most rental mom and pop. Not institutional - won’t sell in a hurry

- 15pc to 20pc increase for new tennants

- Land lost cost of capital increasing to cover higher costs

- Lower vacancy

In Australia - openning up for international students , building costs increasing, limited supply , government support , Airbnb back - will this put a cap on property prices

What does this mean for property prices over next 5 years ?

Wednesday, June 22, 2022

Shares end the 22 EOFY year in Red - But Chant West says don’t panic 😱

Chant West senior investment research manager, Mano Mohankumar, is acknowledging super balances will end the financial year in the red ….

But suggests that people should not panic and sell

Why?

“This is only the fifth decrease in 30 years comes on the back of the outstanding 18 per cent return in financial year 2020/21, the second best in the history of compulsory super.”

You risk missing out when markets rebound – as they will at some point.

Those who switched to cash during the Covid-19 market meltdown missed out on $110,000 in returns by panicking, Chant West’s research showed.

2030 predicted Growth - expectation that cash is not a place to hold your assets long term

A member who had $300,000 in super savings at the beginning of 2020, were projected to have $480,000 in super by the end of 2031 if they stuck with their growth fund.

But a switch to cash in March 2020, would mean they have just $369,000 by the end of 2031.

Subscribe to:

Posts (Atom)