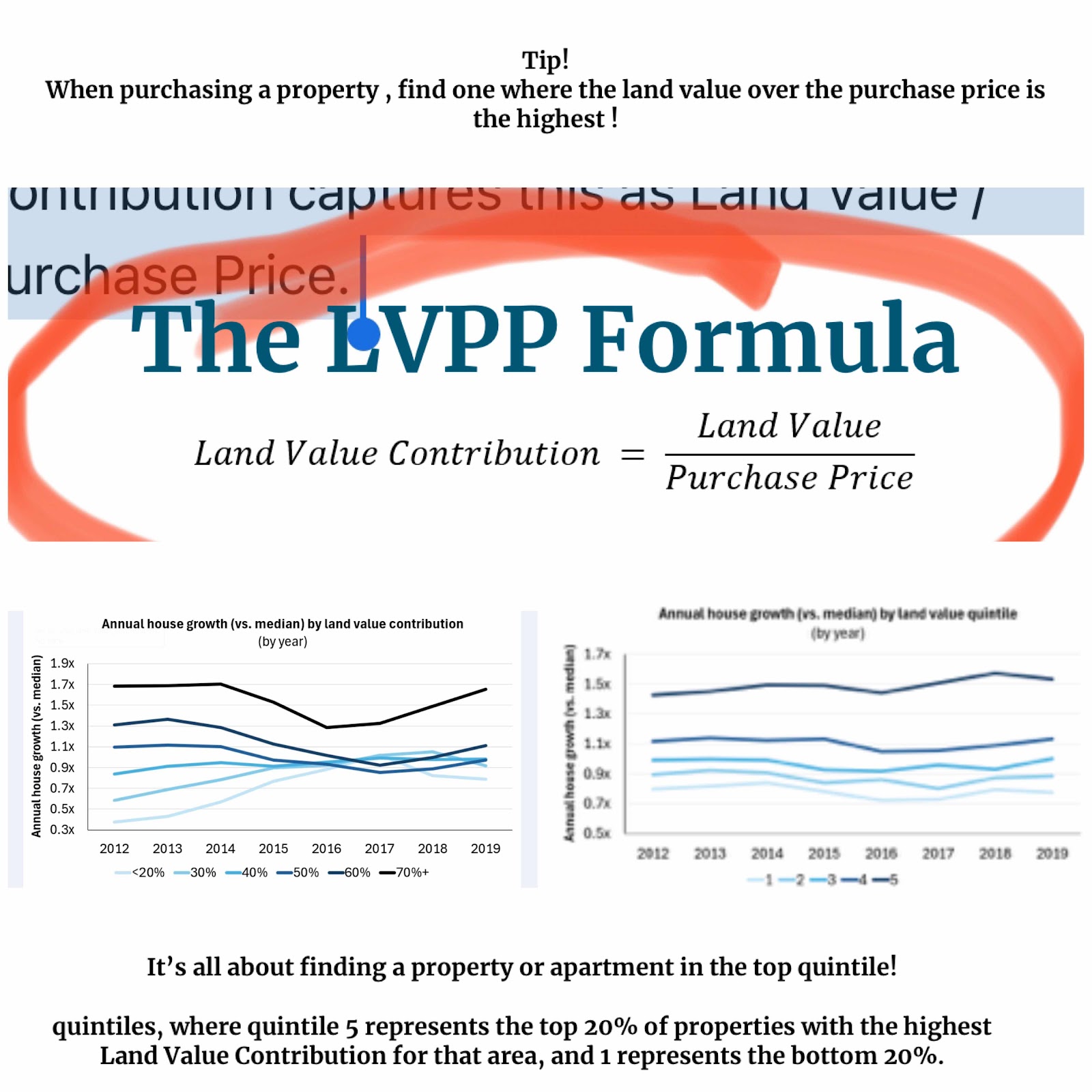

The Help to Buy Scheme is a Labor Government incentive which allows first home buyers (or second home buyers without a current property) to purchase with only a 2% deposit. The Government will then fund and own 30%-40% of the property.

Yes, you have the opportunity to partner with the government to buy your own home!!!

This will then allow the home buyer to get into the market quicker with a lower deposit, lower income, and lower ongoing home loan repayments. The applicant can then choose to buy the Government out at a later date.

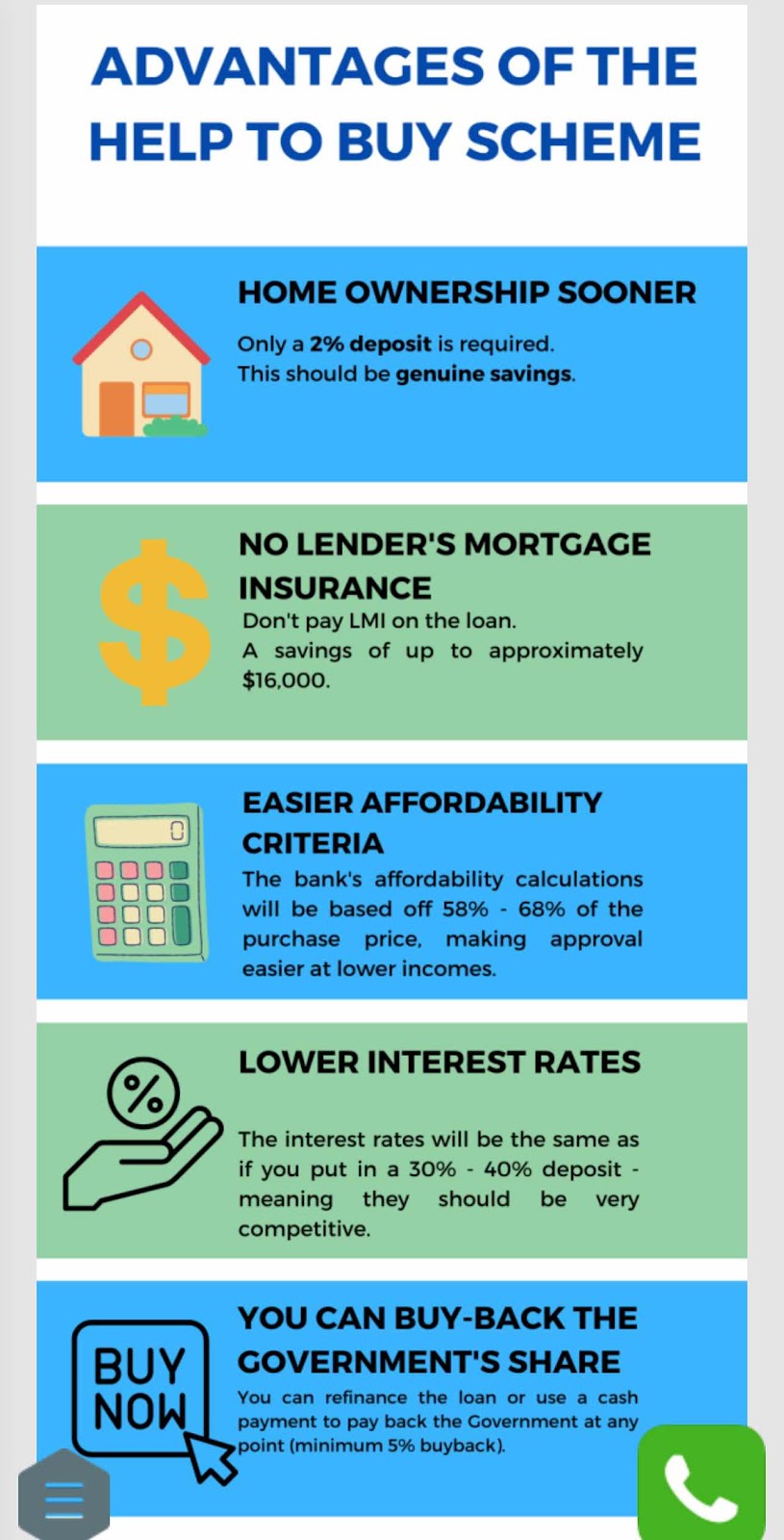

Advantages of the Help to Buy Scheme

The main advantage is that it will get you into home ownership sooner. This can be broken down into a few

points...

Eligibility for the Help to Buy Scheme Australia

Expected eligibility criteria for the Help to Buy Scheme |

Income of less than $90,000 p.a. for a single applicant, or $120k for joint applicants. |

Must be purchasing a property to live in & must not currently own a property in Australia or overseas. |

Must be over 18 years of age. |

Must be an Australian Citizen. |

Must have a 2% deposit. |

There will only be 10,000 spots made available initially.

The Scheme is expected to run for 4 years, with 10,000 spots available each year, for a total of 40,000 spots.

These places will be released to individual participating States & Territories on a per capita basis.

Help to Buy Scheme: Expected start date

The Scheme is expected to start "Early 2024". Although, 01/07/2024 wouldn't be too surprising.

More details on the Housing Australia's Media Release Can be seen here , and Julie Collin's interview on ABC,

They should be releasing the Scheme in early 2024.

If you'd like to be kept updated, please sign up here and type waitlist

How to apply for the Help to Buy Scheme

You currently are unable to apply until it is released.

We will be watching the scheme carefully and contacting all interested applicants as soon as the scheme is ready for release.

If you'd like to be contacted when the scheme is ready, please register here.

We will use this information to keep you updated and to check your eligibility and prepare your submission.

That way we can get you one of the 10,000 spots ASAP and ensure you don't miss out.

Register here for a free service.